Measuring of stream rate in an artist's impression.

In one of our previous publications, we talked about a way to measure event stream rate using a counter based on exponential decay. It turns out that the idea of such a counter has an interesting generalization. This paper by Artem Shvorin and Dmitry Kamaldinov, Qrator Labs, reveals it.

Our immersion plan is as follows. First, let us look at and analyze a few examples of how events are counted and the rate of the stream is estimated in general. The next step is to see a generalization, namely some class of counters, which we call the u-model. Next, we explore what useful properties u-models have and propose a technique for constructing an adequate rate estimate.

1 Examples of Counters

Without limiting the generality, we may assume that an event counter is described by its state

, which, upon the arrival of an event at time

, which, upon the arrival of an event at time  , is updated according to some rule:

, is updated according to some rule:

The state is not necessarily expressed by a number, but for feasibility reasons we may assume that it is representable by a finite set of bits.

In some cases, events are weighted, and the weight of the event

must be taken into account when updating the state:

must be taken into account when updating the state:

But at first, we will consider simple unweighted events, and we will add weight later when we need it. That will not be difficult at all.

In this article, we will limit ourselves to considering only deterministic counters, that is, those for which the update rule is given by a function

. But in general, it may be useful to add some randomness to this mechanism; we recently talked about it [7] and will probably continue to do so.

. But in general, it may be useful to add some randomness to this mechanism; we recently talked about it [7] and will probably continue to do so.It should also be possible, knowing the state of the counter, to estimate the rate of the stream. Generally speaking, the notion of stream rate is non-trivial, and we will discuss it in more detail later. For now, we will just assume that the counter model has some nominal estimate as a function

, written out of some design considerations.

, written out of some design considerations.1.1 Linear Counters: Counting All Events

The simplest thing one may think of is to just count the number of events that have occurred since we started. That is, when an event arrives, we do this:

We will call such counters linear.

The estimate is the average rate over the entire history:

Some problem may occur due to counter overflow. There are also questions about defining the estimate: here, very old events have the same effect on the rate estimate as recent ones.

1.1.1 Sliding Window Event Counting

To eliminate the above drawbacks of linear counters, one may count the number of events not since the creation of the world but only those that occurred no more than

cycles ago. This time interval of length is usually called a window, and it is sliding because it shifts a step forward with each cycle.

cycles ago. This time interval of length is usually called a window, and it is sliding because it shifts a step forward with each cycle.A naive implementation assumes to remember all events in the window, thus requiring

of memory. However, there are ways to save resources in trade-off for reduced precision, such as described in [6]. The update rule is expressed in a rather complicated way, while the average rate over time serves as the estimate:

of memory. However, there are ways to save resources in trade-off for reduced precision, such as described in [6]. The update rule is expressed in a rather complicated way, while the average rate over time serves as the estimate:

Unfortunately, such linear counters are unsuitable for our purposes: we can still tolerate a decrease in accuracy, but

in memory and complexity is too costly, even for small .

in memory and complexity is too costly, even for small .1.2 EDecay: the Exponential Decay

The idea of the decay counter is inspired by the well-known concept of radioactive decay [4]. Its essence is that the amount of undecayed matter decreases over time according to an exponential law:

where

is the amount of matter at the initial (zero) moment of time,

is the amount of matter at the initial (zero) moment of time,  is some parameter, the so-called decay constant.

is some parameter, the so-called decay constant.It is more convenient to rewrite this expression in the following form:

replacing the parameter. For more details on parameterization of counter models, see Section A of the Appendix.

Relying on this mechanism, we can build an event counter as described in our article [1].

By definition, we will assume that each type of event corresponds to the value of, which has a physical meaning of “quantity of matter” and depends on time in such a way that it sharply increases by one at the occurrence of the event and decreases in the remaining time in accordance with the exponential law shown above.

That is, to account for a new event arriving at time

, one must first apply the decay and then increase the counter by one:

where

is the arrival time of the previous event.

is the arrival time of the previous event.To be able to use this, we need to figure out how to store the counter in memory. The simplest way to represent the state of the counter is to use a pair of numbers

, where is the time of the last update, and is the amount of matter at that time. In this case, the update rule and estimation may be written as follows:

, where is the time of the last update, and is the amount of matter at that time. In this case, the update rule and estimation may be written as follows:

In the article [1] we take a detailed look at such counters. An important idea that is relevant to mention here is a lower cost representation of the counter state as a single number

, the so-called absolute value, which holds all the information needed to work with the counter.The value of

Without going into detail, let us just say that with this approach, the update rule and estimation take the form:

1.3 QDecay: a Faster Decay

When looking at the exponential decay model, we can see that the decay function (in this case, the exponent) satisfies the differential equation:

In fact, from a physical point of view, it is instead the other way around: this is the equation describing radioactive decay, and the exponent is its solution.

Indeed, the meaning of the equation is that the rate of decay is proportional to the amount of matter available. At some point, we intended to improve the model making decay faster, so we tried to take a quadratic law (QDecay) instead of a linear one:

The solution is a new decay function:

and it is really gotten steeper.

As a matter of fact…

It is hardly correct to say that a hyperbola is steeper than an exponent. However, large values decay indeed faster (and vice versa for small values).

Similar to the model discussed previously (with exponential decay), here, we can represent the counter state as a single number

. The corresponding update rule and rate estimate look like this:

The great thing here is that calculating the update function is cheap: it requires only elementary arithmetic operations, with only one division. That is, all we originally wanted was a faster horse (faster decay), but we got a new useful feature (cheaper calculations).

We could go further by providing a higher degree in the equation defining the decay function:

and so on, but the solution is more complicated, the calculations are more expensive, and the obvious benefit is somehow not noticeable. Rejected

and so on, but the solution is more complicated, the calculations are more expensive, and the obvious benefit is somehow not noticeable. Rejected1.4 SW: Averaging of Interpacket Interval

Consider another approach to constructing counters, namely averaging. In this case, we will average the time interval between neighboring events. We call this value the interpacket interval, because we deal with network traffic, where the event is the arrival of a network packet, and the word “inter-event” has somehow not caught on.

Generally speaking, the point of this approach is that we have a sequence of values of some quantity (in this case, interpacket intervals) that changes too quickly to be used directly, and we want to smooth or average this sequence in some way.

Averaging is…

Let there be a sequence  , then its average at the

, then its average at the  th step is defined as follows:

th step is defined as follows:

Here, we get the arithmetic mean of the last members of the sequence.

This definition may be generalized. The weighted average of a sequence is the sum

where are some weights such that

are some weights such that  .

.

, then its average at the th step is defined as follows:

Here, we get the arithmetic mean of the last

members of the sequence.This definition may be generalized. The weighted average of a sequence

is the sum

where

are some weights such that .Recall that the newer events are, the more interesting we find their contribution to the rate estimate. So it is natural to use weighted averaging instead of usual averaging, giving more weight to recent events. Weights may be chosen in different ways; now, let us try to take the weights as terms of a geometric progression. This way of summing up is called exponential moving average (EMA).

EMA averaging is…

The exponential moving average of the sequence is defined as follows:

where is a parameter,

is a parameter,  .

.

Since there are very many events, i.e., is large, we may assume that there were some dummy events  ,

,  in the dim and distant past, whose contributions are taken with negligible weights

in the dim and distant past, whose contributions are taken with negligible weights  . Then it is more convenient to rewrite the definition as follows:

. Then it is more convenient to rewrite the definition as follows:

since in this case .

.

One important advantage of EMA over other averaging methods is the ability to collapse a cumbersome sum into a recursive expression:

Thus, it is not necessary to store many old values of for the calculations. By the way, it is the formula (3) is often taken as the definition of EMA [2].

for the calculations. By the way, it is the formula (3) is often taken as the definition of EMA [2].

sequence is defined as follows:

where

is a parameter, .Since there are very many events, i.e.,

is large, we may assume that there were some dummy events , in the dim and distant past, whose contributions are taken with negligible weights . Then it is more convenient to rewrite the definition as follows:

since in this case

.One important advantage of EMA over other averaging methods is the ability to collapse a cumbersome sum into a recursive expression:

Thus, it is not necessary to store many old values of

for the calculations. By the way, it is the formula (3) is often taken as the definition of EMA [2].Applying the exponential averaging formula to the interpacket intervals, we get:

where

is the desired EMA-averaged interpacket interval,

is the desired EMA-averaged interpacket interval,  is the moment when the th event occurs.

is the moment when the th event occurs.This model is mentioned again in Section 4.3, where, in particular, we show how to express the counter state by a single number and simplify the calculations. For now, let us just write out the result.

Update the counter when an event occurs at time

:

The reciprocal of the averaged interpacket interval serves as the rate estimate:

Remark

Using EMA averaging, we can also obtain a model exactly coinciding with the decay model from Section 1.2. Instead of averaging the interpacket intervals, this deals with the value  , which could be called the momentary rate:

, which could be called the momentary rate:

, which could be called the momentary rate:

1.5 Probabilistic Counters

The idea of probabilistic counters is to change the counter state when an event arrives, not always, but with some probability. This probability may be defined in various ways, e.g.

- stay constant (binomial counters);

- decrease by a factor of 2 after each successful update (Morris counters);

- change after every

of successful updates.

of successful updates.

Probability counters make very efficient use of memory. For example, the original 8-bit Morris counters may be used to account for up to

events. Their obvious disadvantage, however, is significant inaccuracy in estimating the number of events. We discuss such counters in detail in the article [7], and we also propose some extensions of known algorithms.

events. Their obvious disadvantage, however, is significant inaccuracy in estimating the number of events. We discuss such counters in detail in the article [7], and we also propose some extensions of known algorithms.2 The Idea of the U-model

If we look at the counters based on the idea of decay, we may notice this peculiarity: the state is described by a pair of numbers

, but then it miraculously appears to be possible to express the state by a single number . Let us try to find a general principle by which this becomes possible for any counters of this type.

, but then it miraculously appears to be possible to express the state by a single number . Let us try to find a general principle by which this becomes possible for any counters of this type.Let us temporarily forget the fact that in practice, the counter value must be discrete and represented by a relatively small number of bits, and, staying within the spherical cow concept, let us assume both the counter value and the event arrival time be real numbers, and the transformations over them also are real-valued functions. Later (see Section 3.3) we will learn how to discretize the models, making them usable in practice.

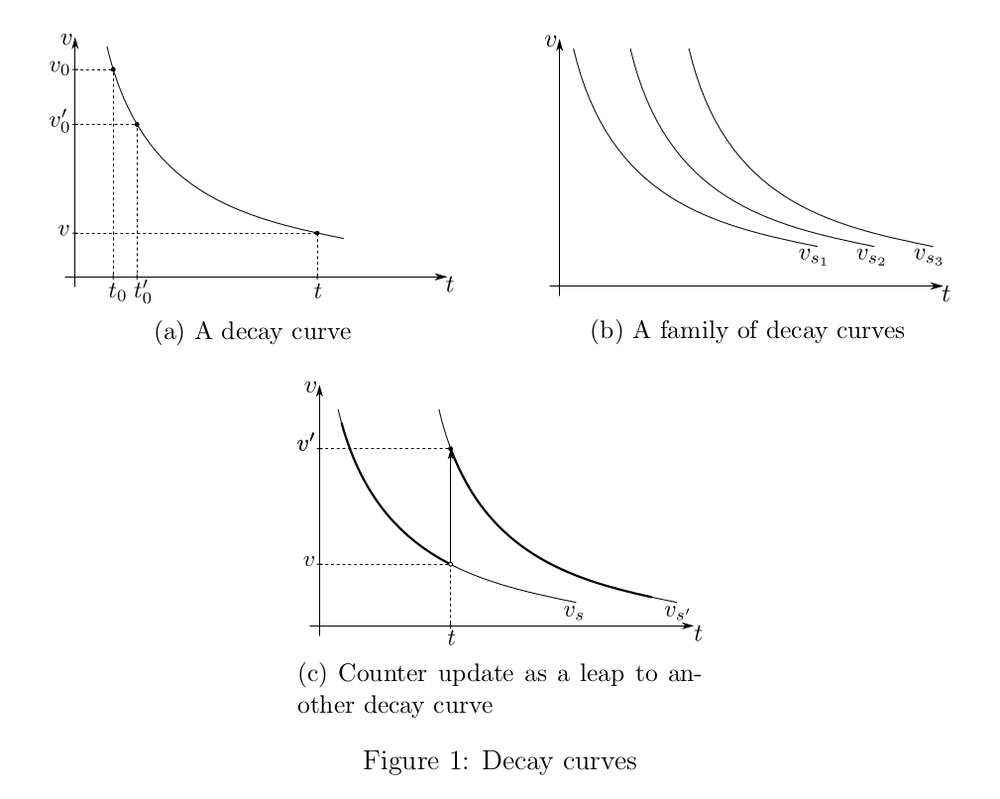

2.1 An Invariant of Decay

Consider a section of the decay curve (see Fig. 1a). Let at time

an event was registered, and then on the interval  there were no other events. Now we are at the point going to account for a new event, or just to see what the value of is, in order to estimate the rate. One may notice that from the point of view of an observer at the moment there is absolutely no difference whether the last event occurred at the

there were no other events. Now we are at the point going to account for a new event, or just to see what the value of is, in order to estimate the rate. One may notice that from the point of view of an observer at the moment there is absolutely no difference whether the last event occurred at the  point on the plot or at

point on the plot or at  . This fact seems to hint that storing two numbers as the counter state is redundant. Thus, the two formally different versions of reality are functionally equipotent. That is, they give the same effect:

. This fact seems to hint that storing two numbers as the counter state is redundant. Thus, the two formally different versions of reality are functionally equipotent. That is, they give the same effect:

Generally speaking, we do not have a single decay curve, but a family

(see Figure 1b). Each of these curves describes a state of the counter. They may be enumerated somehow, and we may take the index of the curve as the counter state.

(see Figure 1b). Each of these curves describes a state of the counter. They may be enumerated somehow, and we may take the index of the curve as the counter state.Let us now see how such a counter should be updated. Let

be the current state of the counter. According to the decay model, this means that in the absence of events, the value of changes over time, remaining on the curve  . Let an event occur at some point . This means that the value of increases stepwise by one (see Fig. 1c), that is, among the whole family of curves we must find the one that passes through the point

. Let an event occur at some point . This means that the value of increases stepwise by one (see Fig. 1c), that is, among the whole family of curves we must find the one that passes through the point  where

where  . Let

. Let  be the index of the found curve, i.e.,

be the index of the found curve, i.e.,

then this is the value of

to set as the new counter state.

Remark

If one wants to count weighted events, the stepwise change should be not by one but by the weight of the event:  .

.

.It is not yet clear how to find the index of the desired curve, but it will come to light very soon.

2.2 Translational Symmetry

In Fig. 1b decay curves

are depicted in such a way that they differ from each other only by a horizontal shift. Scientifically, this is called translational symmetry of the time [8]. We want to take this property as an axiom for our counter model. Indeed, it is logical to expect that, within the model, the decay process goes today in exactly the same manner as it did yesterday.Mathematically, this property may be written as follows:

that is, the curve

is obtained from the curve

is obtained from the curve  by shifting it to the right by some

by shifting it to the right by some  .

.In general, curves may be enumerated any way you like, and you just need to be able to find the index of the new curve during the update operation. But it is more convenient to enumerate them in order so that the index

represents something meaningful, namely, a real number corresponding to the horizontal distance between the curve and the curve with zero index  . Then, due to translational symmetry, any curve from the family may be very simply expressed as a shift of the curve number zero:

. Then, due to translational symmetry, any curve from the family may be very simply expressed as a shift of the curve number zero:

Remark

Here we introduce the notation  , which is convenient because the function

, which is convenient because the function  increases monotonically. This will come in handy later in Section 2.4 in determining the rate.

increases monotonically. This will come in handy later in Section 2.4 in determining the rate.

, which is convenient because the function increases monotonically. This will come in handy later in Section 2.4 in determining the rate.Now, the update rule on an event arrival at time

may be expressed from equation (5) as follows:

Thus, the update rule appears as

where

is some function.

is some function.This rule looks so simple and universal that it may be taken as the definition. That is how we will define the u-model.

Remark

If the decay function is given by a differential equation of such kind:

then it is always easy to find an invariant for that the property (6) holds.

Indeed, the solution of the differential equation may be written as

Thus we can take as an invariant, and the corresponding curve is expressed as

as an invariant, and the corresponding curve is expressed as  .

.

then it is always easy to find an invariant for that the property (6) holds.

Indeed, the solution of the differential equation may be written as

Thus we can take

as an invariant, and the corresponding curve is expressed as .Section 3.1 lists the formal properties that the function

must satisfy in order to build a workable counter model on its basis.

must satisfy in order to build a workable counter model on its basis.2.3 Absolute and Relative

We may say that

is the absolute value of the counter, it is stored directly in memory, and  is the relative value of the counter at time . Then it turns out that the update function works with the relative counter value:

is the relative value of the counter at time . Then it turns out that the update function works with the relative counter value:  .

.The fact that the update function works with the relative counter value reflects the decay principle: if no events occur, then the absolute value of

does not change, and the relative value automatically decreases over time. And the rate estimate, accordingly, also degrades. From the calculation point of view, it is very convenient: as long as there are no events, there is no need to do anything. It is very similar to inflation in economics: the state of the counter stands for banknotes lying under the pillow, and the rate estimate stands for the purchasing power of these banknotes, which degrade itself.2.4 Rate Estimate

For the decay model, the value

by construction is the rate estimate, see formula (6). However, several problems arise with this definition. First, if we use the definition of the model through the function , it would be difficult to construct the function (the functional equation (7) would be needed to solve). Secondly, it would be nice to check experimentally how adequately a particular counter measures the rate.

by construction is the rate estimate, see formula (6). However, several problems arise with this definition. First, if we use the definition of the model through the function , it would be difficult to construct the function (the functional equation (7) would be needed to solve). Secondly, it would be nice to check experimentally how adequately a particular counter measures the rate.Preserving not the letter (from the formula (6)), but the spirit of the decay idea, we construct the rate estimate as a function of a single argument, namely, the relative value of the counter:

. Thus, the problem is set as follows: having an update function

. Thus, the problem is set as follows: having an update function  , construct a function

, construct a function  that would be an adequate estimator of the rate.

that would be an adequate estimator of the rate.It turns out that the u-model approach consists of implementing the following plan (yes, it looks a bit punkish).

- We take some models built from “physical considerations”, and for each of them, we express the update rule through a u-function.

- Then we abstract away from the physical sense, leaving only the bare u-function. Now we can, without worrying about the sense, boldly change the u-function, for example, by choosing a computationally cheaper one.

- Finally, we figure out how to reintroduce meaning, i.e., to construct an adequate estimate of the rate.

- PROFIT!

In order to make this plan possible (the snag, obviously, is only clause 3), some constraints on the u-function would have to be imposed, and now let us try to figure out which ones. The reader, however, may skip these motivational considerations and jump directly to the definition of those constraints (9) on the u-function in Section 3.

2.4.1 A Uniform Stream

Our company studies network traffic, and we may need to count network packets arrivals as items. In this case, they form a stream, and its rate is measured in packets per second (pps). Alternatively, we have to take packet size into account, so the size is considered the weight of an event, and correspondingly, the rate of such a weighted stream is measured in bits per second (bps). It may also be important to distinguish packets by their contents (source and/or destination IP address, port number, protocol, etc.), then we group events by their type and create separate counters for each type.

Since we discuss here how to evaluate the rate of an event flow, we must first formalize the notions of the event and the event stream.

Definition (event). Let us call an event a triple, where

is the event weight,

is the event type, some stream identifier.

Definition (event stream). An event stream is defined as a sequence of events,

. And the events in the stream must be ordered by time:

at

.

In most implementations of event accounting systems, the time is considered a discrete value:

, but for theoretical reasoning, it may be convenient to generalize and consider the time continuous:

, but for theoretical reasoning, it may be convenient to generalize and consider the time continuous:  .

.If we are interested only in events as such, e.g., we measure the number of packets in pieces per second, then the weight

may be assumed to be unity. It is also assumed that a single counter counts events of the same type, i.e., the field serves to distinguish different streams and does not play a role within a single counter.Definition (uniform stream). A deterministic uniform streamis defined as follows:

Whereis the stream parameter, i.e., the period between events. Then the rate of such a stream, by definition, is expressed as

.

Now we can express a way to measure the stream rate for any model. Consider a stream of some known rate

affecting a counter and observe how the relative value of the counter changes; let the measured counter value be

affecting a counter and observe how the relative value of the counter changes; let the measured counter value be  after the th event.

after the th event.We want the stream rate

and the sequence of values to be somehow related. Then, being lucky, we could construct a rate estimation function .2.4.2 An Attractor

Studying with concrete examples the behavior of the u-model under the influence of a deterministic stream, we found that (at least for those examples) there is a notion of an attractor, which is somewhat informally described by the following properties.

- For every rate value of the incoming stream , there exists an attractor, i.e., such a subset of the relative counter values that if any value

ended up in this attractor, then all subsequent values for

ended up in this attractor, then all subsequent values for  will also end up there. The attractor is an interval

will also end up there. The attractor is an interval ![$[\check{x}, \hat{x}]$](https://habrastorage.org/getpro/habr/formulas/da4/859/d9d/da4859d9d269da5f46015f7f1899f87c.svg) (possibly degenerate, when both ends of it have merged).

(possibly degenerate, when both ends of it have merged). - There is convergence: even if the relative value of the counter was outside the attractor, after several updates, it will get there or at least get as close to the attractor as possible.

- There is monotonicity: the position of the attractor depends monotonically on the rate of the incoming stream. That is, both ends of the segment

and

and  are monotonically increasing functions.

are monotonically increasing functions.

Since we need to judge the rate of the stream by the value of the counter, we need to solve the inverse problem. This is possible due to monotonicity and continuity: there exist functions

such that if

such that if  enters the attractor, we can guarantee that the true rate value lies in the interval

enters the attractor, we can guarantee that the true rate value lies in the interval ![$[\check{r}(x), \hat{r}(x)]$](https://habrastorage.org/getpro/habr/formulas/bc7/c31/0be/bc7c310bec58b9eabfb6bf48bf04bb37.svg) .

.Of course, for these properties to be practically useful, first, the segment (attractor) must be short; otherwise, the accuracy will be low, and second, the convergence must be fast, or one will have to wait for a long time before the counter starts to show an adequate value. In any case, for a particular u-model, it is possible to write down the solution explicitly and evaluate the accuracy and speed of convergence.

Let us try to pass from the particular to the general. Now, ask a question: What conditions must be imposed on the u-function for the corresponding u-model to have an attractor with the above properties? An exhaustive answer is given in the next section.

3 Implementation of the U-model

3.1 Definition of the U-model

Let the function

satisfy the following conditions:

satisfy the following conditions:

where

.

.Definition (u-model). Consider a counter update method based on the function

having the properties (9), in which the counter update

event arrival at timeis expressed by the rule (8):

This way of updating the counter will be called the u-model.

A function

satisfying the conditions (9), has some useful properties. For example, the function (and also  ) is continuous. This arises from the properties (9a) and (9c) having used the

) is continuous. This arises from the properties (9a) and (9c) having used the  -

- -formalism. Second, either

-formalism. Second, either  on

on  , or there exists such

, or there exists such  that at

that at  , and

, and  at

at  .

.3.2 Rate Measurement

Properties (9) are sufficient to ensure the existence of an attractor and to construct upper

and lower

and lower  estimates of the rate. There are several theorems on this point, some of which are presented in this section and some of which are left out.

estimates of the rate. There are several theorems on this point, some of which are presented in this section and some of which are left out.3.2.1 A Strict U-model

We can observe that the conditions (9) do not forbid the case when the increment of the update function converts to zero at some point, that is, when

. In this case, will also convert to zero at all

. In this case, will also convert to zero at all  . Let us denote by

. Let us denote by

It is easy to prove that if we take

and apply a series of updates to it, then values larger than

and apply a series of updates to it, then values larger than  will be unattainable, so the relative counter values will never go beyond

will be unattainable, so the relative counter values will never go beyond  . That is,

. That is,  may be called the operating range of the u-model. Outside this range, the u-function is arranged trivially, and we are not interested in its behavior. This caveat is needed to introduce the notion of a strict u-model.

may be called the operating range of the u-model. Outside this range, the u-function is arranged trivially, and we are not interested in its behavior. This caveat is needed to introduce the notion of a strict u-model.Definition (strict u-model). If, in addition to the properties (9) functions

Theorem (fixed point theorem). For a strict u-model under the influence of a deterministic uniform rate streamsuch that

.

This directly follows from the Banach fixed-point theorem [5], which guarantees the existence and uniqueness of a fixed point in a compressible mapping. Then all terms of the sequence

will be equal to the value of this fixed point.It turns out that in a strict u-model, the attractor consists of a single point.

In fact, not for all u-models we use the update function is a compressible mapping. For example, the EDecay model has an “almost” compressible update function, as for it, the constant

is equal to one. That means the Banach theorem does not work. But this is not a problem from the practical application point of view because there are other useful theorems.

is equal to one. That means the Banach theorem does not work. But this is not a problem from the practical application point of view because there are other useful theorems.For example, the following statement holds.

Statement. If at some point in time the counter was in a state where its relative value was, and a deterministic stream of events began to arrive at it, then the sequence of its relative values

tends to some value of

, and the convergence rate is known. In particular, for the EDecay model, the convergence looks like this:

, which, from a practical point of view, allows us to evaluate how quickly and adequately the model responds to changes in the traffic pattern.

3.2.2 A Non-strict U-model

As for discretized models (see Section 3.3), they lose strict monotonicity, so instead of the fixed point theorem, a set of assertions (not given here) that require weaker conditions and give weaker, though still useful, results for rate estimation helps. For the non-strict model, instead of a one-to-one correspondence between the rate of the stream and the relative value of the counter, there is an interval estimate. That is, the attractor is a nondegenerate segment.

Using the proposed methodology, for a given u-model, all that remains is to construct upper

and lower estimates of the rate and find out how rapidly the sequence converges to the attractor.3.3 Discretization

In order to use the u-model in practice, it must be discretized. That is, to make the set of counter states finite and preferably small in size. Why small? We need to keep billions of counters in memory; the more of them, the higher will be the quality of service. Indeed, why should we waste 64 bits per counter when we can do with 16?

Remark

One may go for the trick of complicating the state representation by assuming it as a pair  , where

, where  refers to a particular counter, and

refers to a particular counter, and  is the common part of the state of a whole group of counters. We do use this technique, in particular, to deal with counter overflows, but we do not consider it in this paper.

is the common part of the state of a whole group of counters. We do use this technique, in particular, to deal with counter overflows, but we do not consider it in this paper.

, where refers to a particular counter, and is the common part of the state of a whole group of counters. We do use this technique, in particular, to deal with counter overflows, but we do not consider it in this paper.One obvious way to discretize is to select a finite subset of consecutive integers from the continuum of relative counter values and modify the u-function slightly to become an integer.

First, let us construct a function

such that:

such that:- it has integer values at integer points:

for

for  ,

, - is in some sense close to :

for ,

for , - satisfies the conditions (9).

Apparently, this problem may be solved in different ways. Below is one particular way of constructing

.

.The basic idea of this construction is to set the values of

at integer points by rounding down, that is,  for , then complete at intermediate points so that continuity and monotonicity (conditions (9)).

for , then complete at intermediate points so that continuity and monotonicity (conditions (9)).It is more convenient to first construct

and then determine through it. To do this, fix at integer points, and do linear interpolation at intermediate points. That may be written as follows:

and then determine through it. To do this, fix at integer points, and do linear interpolation at intermediate points. That may be written as follows:

where

are the integer and fractional parts of the argument, respectively.

are the integer and fractional parts of the argument, respectively.All that remains is to determine the function

itself:

itself:

Statement. The function

Remark

Generally speaking, the u-model gets a bit screwed up with this operation (switching from to ): if it was strict, it ceases to be so after the transformation.

to ): if it was strict, it ceases to be so after the transformation.A legitimate question arises: why do we need to add

at intermediate (non-integer) points if we plan to perform calculations only over integer counter values? The point is that in addition to the update rule, we need to build another rate estimate, and the easiest way to do that is to apply a “lazy approach”: first, extend at non-integer points, gaining a new u-model, then use theorems relating the observed counter value to rate estimates, thus reducing the problem to the solved one.

Remark

There seems to be some meta theorem to claim that, regardless of the way is constructed at intermediate points, the methodology for constructing the estimates gives the same result.

is constructed at intermediate points, the methodology for constructing the estimates gives the same result.Now we have a function

that generates a u-model and takes integer values at integer points. It remains to take care of limiting it on a finite interval, so that the counter values do not spread to infinity. To do this, take the integer interval  and limit on it, that is, we get a function

and limit on it, that is, we get a function  that matches on the area of definition.

that matches on the area of definition.

How to choose the interval bounds

Take as such a number that  ,

,  . (By virtue of the condition (9d), such a number exists.) Then the result of the update will never exceed the right bound: for

. (By virtue of the condition (9d), such a number exists.) Then the result of the update will never exceed the right bound: for  we have

we have  . As for the left boundary, it may be chosen arbitrarily (any

. As for the left boundary, it may be chosen arbitrarily (any  will do). Indeed, due to non-negativity of

will do). Indeed, due to non-negativity of  for ,

for ,  will be satisfied, that is, the result of the update will not exceed the left boundary. Thus,

will be satisfied, that is, the result of the update will not exceed the left boundary. Thus,  may be chosen based on counter size considerations: the larger the counter capacity, the more left-hand boundary may be moved, and the more accurate the estimate of low-intensity streams will be.

may be chosen based on counter size considerations: the larger the counter capacity, the more left-hand boundary may be moved, and the more accurate the estimate of low-intensity streams will be.

such a number that , . (By virtue of the condition (9d), such a number exists.) Then the result of the update will never exceed the right bound: for we have . As for the left boundary, it may be chosen arbitrarily (any will do). Indeed, due to non-negativity of for , will be satisfied, that is, the result of the update will not exceed the left boundary. Thus, may be chosen based on counter size considerations: the larger the counter capacity, the more left-hand boundary may be moved, and the more accurate the estimate of low-intensity streams will be.It is this function

(more precisely, its numerical implementation) that we will use in the counter update algorithm.

(more precisely, its numerical implementation) that we will use in the counter update algorithm.Section B of the Appendix shows the discretization of the EDecay model as an example.

4 Examples of U-model Counters

As shown above, the counters introduced in Section 1 (except for linear ones) are represented as u-models. Here we consider them again, now as u-models: first, take the u-function, then construct the estimators.

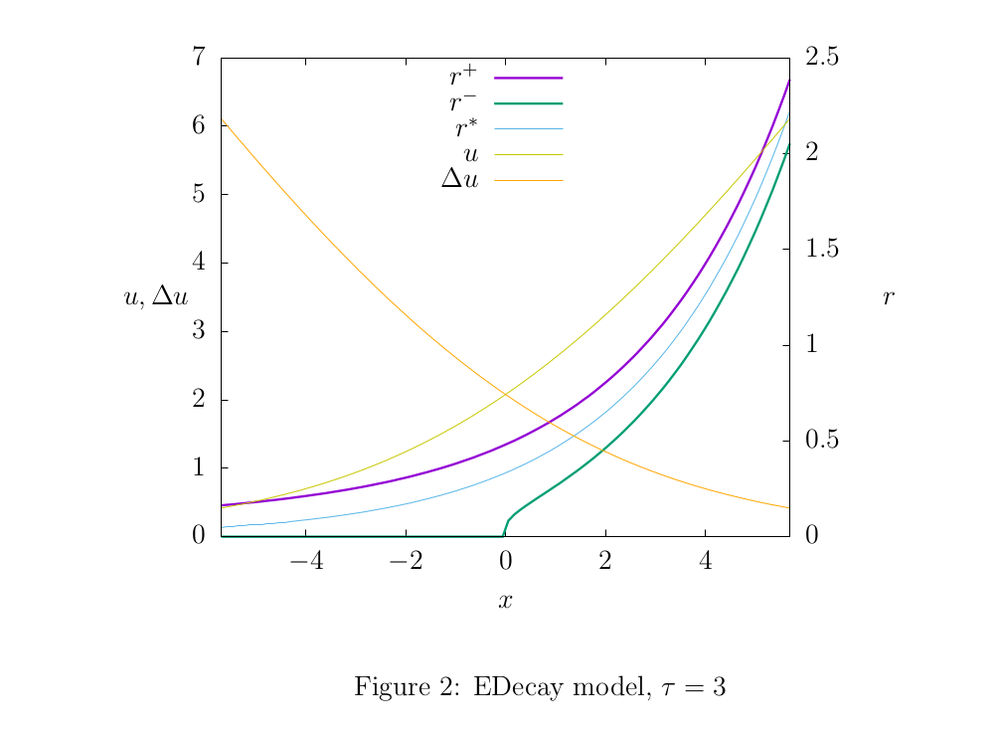

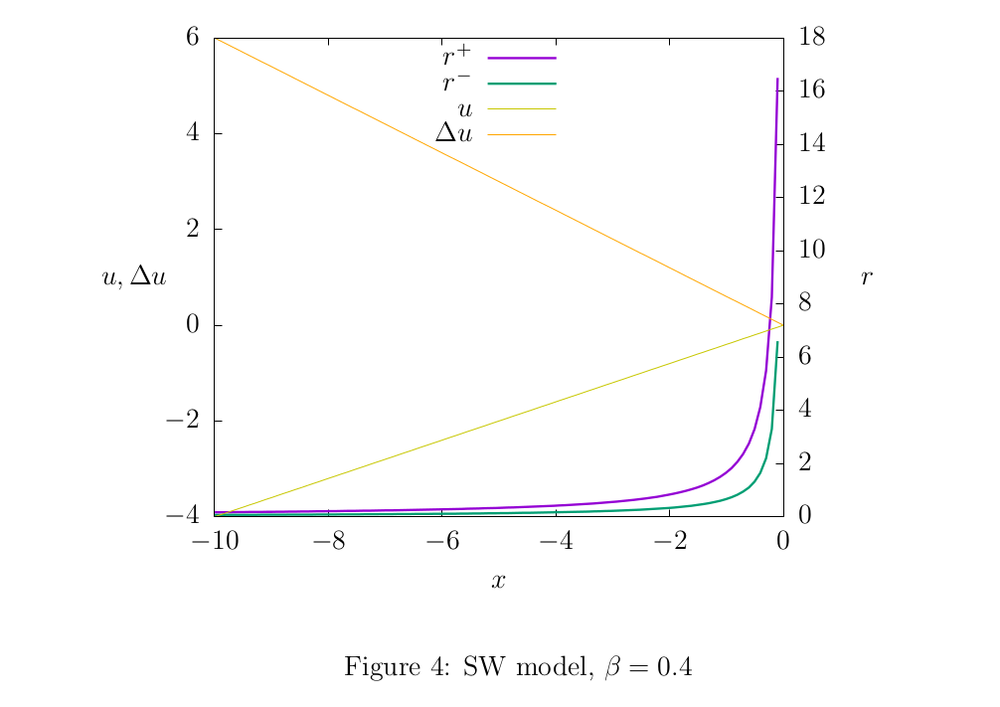

Figures 2,3, and 4 illustrate the properties of the models: shades of yellow show the function graphs

and  , and the remaining graphs are rate estimates. The parameters of the models were chosen in such a way as to show the difference between the upper and lower estimates. In practice, we use such parameter values so that the estimates are more accurate. If, for example, for the EDecay model we take

, and the remaining graphs are rate estimates. The parameters of the models were chosen in such a way as to show the difference between the upper and lower estimates. In practice, we use such parameter values so that the estimates are more accurate. If, for example, for the EDecay model we take  larger (for example, in our working code is about

larger (for example, in our working code is about  ), the graphs of the estimates will visually merge, which obviously indicates the high accuracy of the model.

), the graphs of the estimates will visually merge, which obviously indicates the high accuracy of the model.4.1 EDecay

The update rule (1) looks like this:

where

is a parameter (see Section A of the Appendix).

is a parameter (see Section A of the Appendix).This model has an interesting feature: there is an estimating function

(its graph is indicated by the blue line in Fig. 2), which has the following property. Let there be two counters that account for two different event streams and a third counter that accounts for both streams at once. Then for the EDecay model, there exists an estimator function

(its graph is indicated by the blue line in Fig. 2), which has the following property. Let there be two counters that account for two different event streams and a third counter that accounts for both streams at once. Then for the EDecay model, there exists an estimator function  such that at each time the equality holds:

such that at each time the equality holds:

where

and

and  are the absolute value of the first two counters, and is the absolute value of the third. It makes sense to call this property of the model additivity. It turns out that EDecay is the only one among all u-models that has this property. For other u-models, this equality can be satisfied only approximately. Here, by the way, there is a clear analogy with radioactive decay: we may say that this estimate plays the role of mass or amount of matter.

are the absolute value of the first two counters, and is the absolute value of the third. It makes sense to call this property of the model additivity. It turns out that EDecay is the only one among all u-models that has this property. For other u-models, this equality can be satisfied only approximately. Here, by the way, there is a clear analogy with radioactive decay: we may say that this estimate plays the role of mass or amount of matter.4.2 QDecay

The corresponding rule (2) the update function looks like this:

4.3 SW

The update rule (4) is equivalent within the u-model through the update function

A useful property of this model is the computational simplicity of the update function; we can directly write this formula into code without any table approximations.

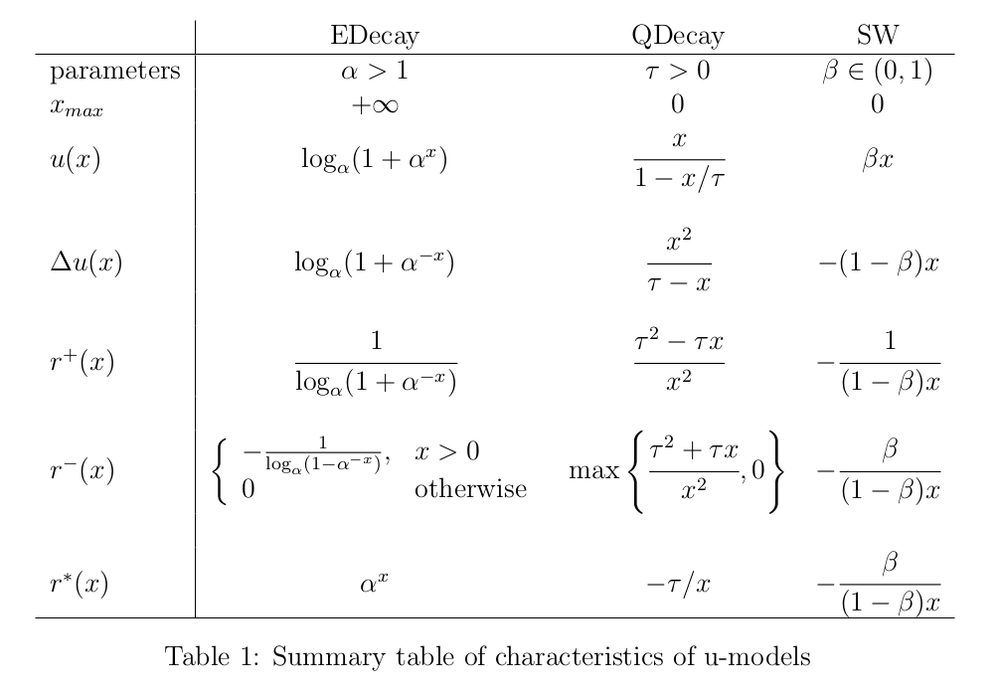

4.4 Summary Table

Table 1 lists the characteristics of the mentioned models.

One may notice that for some models, the formula for the lower estimate

becomes meaningless at some values of the argument. That means that for such (too small) relative counter values, we cannot say anything about how small the rate may be, so we assume that the lower estimate simply equals zero (no rate is less than zero). Theoretically, for some u-models, it may happen that the upper estimate

becomes meaningless at some values of the argument. That means that for such (too small) relative counter values, we cannot say anything about how small the rate may be, so we assume that the lower estimate simply equals zero (no rate is less than zero). Theoretically, for some u-models, it may happen that the upper estimate  makes no sense for some reason. In such cases, it should be assumed to be infinite.

makes no sense for some reason. In such cases, it should be assumed to be infinite.In addition to the rigorous rate estimates

and derived from the general u-model methodology, an estimate of  constructed “from physical considerations” (the blue line in the graphs) is also indicated. It was expected that it would always be between the lower and upper estimates ( and ), but with the QDecay model, this is not the case, as there is an area where it is smaller than the lower estimate. This example shows the usefulness of the approach described here: whatever the considerations on which the counter model is built, it is always useful to double-check how a stream of a known rate affects the state of the counter.

constructed “from physical considerations” (the blue line in the graphs) is also indicated. It was expected that it would always be between the lower and upper estimates ( and ), but with the QDecay model, this is not the case, as there is an area where it is smaller than the lower estimate. This example shows the usefulness of the approach described here: whatever the considerations on which the counter model is built, it is always useful to double-check how a stream of a known rate affects the state of the counter.Conclusions

The general principles of event counters have been shown in several examples. As a rather universal generalization, the u-model scheme has been proposed. A methodology for constructing rate estimates for any u-model has been proposed.

In addition, a lot of interesting things were left out of the picture.

- Probability Counters. What happens if we replace the function in the u-model update rule with a random variable that depends on the relative value of the counter?

- Representation and maintenance of large arrays of identical counters. The update and evaluation functions depend on the relative counter value , where and may be in a relatively narrow range of values, while runs over a wide (potentially infinite) range. How can we make sure that the counters do not overflow?

- Algorithms detecting heavy streams. Individual counters allow us to measure the rate of streams, but how do we organize them to reveal the most intense streams?

Appendix

A Parameterization

All of the counter models discussed in this article are single-parameter. But we use different values in different places to make the formulas look more convenient. Below is a list of quantities that may be equally used as a model parameter, with an indication of their physical meaning and the relationship between them.

is the so-called decay constant from the law of radioactive decay [4]

is the so-called decay constant from the law of radioactive decay [4]

,

,  is a value characterizing the average lifetime in the same model. It is also true that during the time the amount of decaying matter decreases

is a value characterizing the average lifetime in the same model. It is also true that during the time the amount of decaying matter decreases  times, and the half-life is expressed through as follows:

times, and the half-life is expressed through as follows:  .

. ,

,  .

.- is the smoothing parameter in the EMA [2]

The exponential decay model may be expressed in two ways: through radioactive decay and through EMA smoothing. Here is the relationship between these parameters: .

.

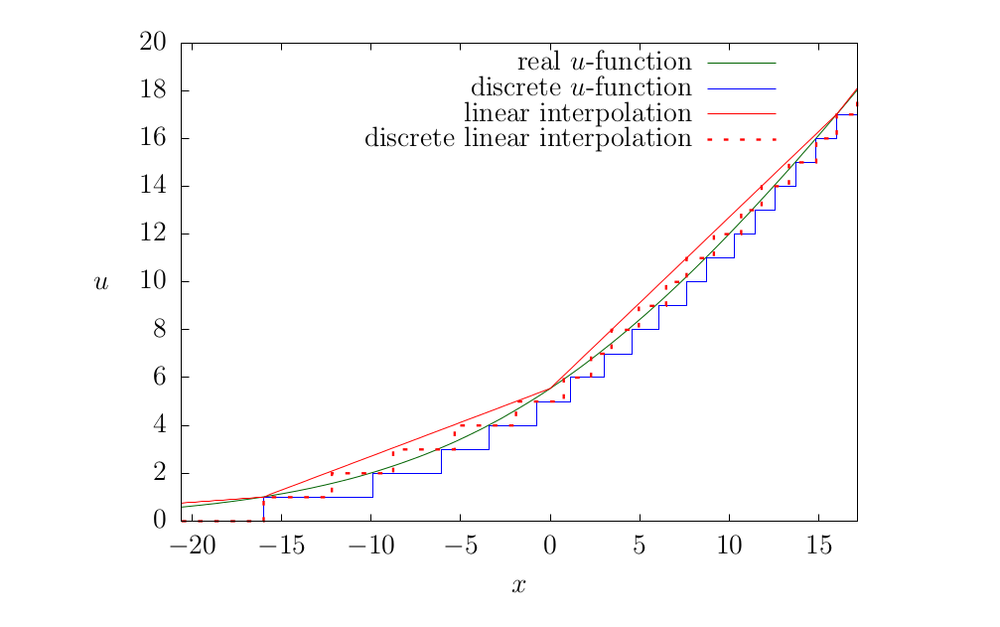

B An Example of EDecay Discretization

The EDecay model is defined by the following update function:

Consider in Fig. 5 how the update function changes with sampling.

- There is a perfect real-valued update function that exactly exponential decay model (the smooth green line in the graph).

- It has to be discretized for practical applications. It is possible to use a floating-point representation (obviously, it is also discretized, only not uniform) or take an integer representation. In this case, rounding down applies, although it is not crucial (blue line).

- Finally, It is possible to overload the update function even more. In [1] to speed up calculations, it was suggested that instead of calculating the real-valued function with logarithms and exponents, a table approach should be used. It was assumed that the size of the table would be small if a low-digit counter was used. However, nothing prevents us from thinning the table by reducing its size a few more times and implementing linear interpolation. The resulting update function will be slightly different (the red dotted line on the graph).

Of course, as a result of sampling, the update function is distorted, which is not a problem in itself, but we have to take it into account when constructing the rate estimate. In addition, strict monotonicity of the model is inevitably lost, which reduces the accuracy of the estimate. The degree of distortion depends on the parameter

: the larger it is, the closer the discretized function is to the original one.References

[1] Our article about the decay model: https://qratorlabs.medium.com/rate-detector-21d12567d0b5

[2] Exponential moving average: https://en.wikipedia.org/wiki/Moving_average#Exponential_moving_average

[3] Weighted moving average: https://en.wikipedia.org/wiki/Moving_average#Weighted_moving_average

[4] The radioactive decay law: https://en.wikipedia.org/wiki/Exponential_decay

[5] Banach fixed-point theorem: https://en.wikipedia.org/wiki/Banach_fixed-point_theorem

[6] Ayur Datar et al. — Maintaining Stream Statistics Over Sliding Windows — Society for Industrial and Applied Mathematics, Vol. 31, No. 6: http://www-cs-students.stanford.edu/~datar/papers/sicomp_streams.pdf

[7] Our overview of Morris's counters: https://habr.com/ru/company/qrator/blog/559858/

[8] Translational symmetry: https://en.wikipedia.org/wiki/Translational_symmetry